Search Bull Run

When Fear Disconnects From Fundamentals: A Rare Entry Point in AI and Software

February 3, 2026

.png)

Recent market action in AI and software has been driven far more by sentiment than by fundamentals. The current sell-off in our AI-focused Innovation Portfolio and software-focused Growth Portfolio reflects fear and crowded positioning, not deterioration in underlying business performance. In our view, this has created one of the most compelling buying opportunities since the April 2025 pullback.

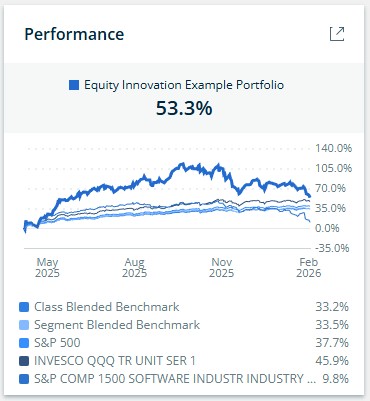

Since the April low of last year, our Innovation portfolio has returned 53.3%, gross of fees, vs 37.7% for the S&P 500, 45.9% for the Nasdaq 100, and 9.8% for the S&P 1500 Software Index, as of 2/25/26:

Last Fall (Fall 2025), the general market narrative was one of lingering concern: AI was a momentum trade due for a correction, and the Software sector was still seen as lagging. Yet, today, even as the positive news is pouring in, both sectors are being indiscriminately sold. For example, a leading AI chip company like AMD recently reported strong earnings, and their CEO, Lisa Su, has stated that demand is even greater than she had expected just six months ago (CNBC video). Despite this overwhelmingly positive signal on the core of the AI theme, the stock is down.

This level of disconnect often leaves market commentators exasperated, with Jim Cramer this morning noting that the pervasive fear has led to a point where "I guess we have to restart thinking about what people like". This sarcarsm captures the current mood: when fear takes over the market, and there is all this doom talk, it doesn't feel good to buy—but that is precisely the moment of maximum opportunity.

Facts and Figures: Innovation Portfolio Strength

This recent decline is a textbook "shakeout" that is forcing out weak hands and creating an entry point at historically cheap valuations for high-growth assets.

Here is a look at the current opportunity and portfolio's track record:

- Valuation: Our holdings across Innovation and Growth are currently trading at a great discount. High-growth stocks are "extremely cheap" right now, with Software multiples at some of the cheapest levels we have seen in a very, very long time. The risk of a major valuation collapse is nearly impossible, as current multiples have already fallen well beyond historically depressed levels.

- Historical Opportunity: The current 10% pullback in our portfolio YTD is a classic example of the kind of market dip that has historically been an excellent buying opportunity. When the Nasdaq-100 has pulled back 5%–10% from all-time highs, the forward returns have been extremely strong, averaging +24.3% in one year.

- ARKW as a Proxy: Our Innovation Portfolio’s performance and current drawdown align closely with high-growth ETFs like ARKW, which is down about 25% from its peak. ARKW itself has returned 7.79x on investor capital since 2014. The recent moves in our Innovation Portfolio holdings, which include key growth themes like AI and Software, are directly comparable to this growth-focused proxy.

- Since launching in 2020, our Innovation Portfolio has closely matched ARKW’s performance, and we believe our smaller size will allow us to sustain our historical growth over time by investing flexibly without market impact or capital constraints.

BRIM Equity Innovation Portfolio (net of fees) vs ARKW vs S&P 500 Past 3 Years:

Long-Term Outlook: Strong Growth & Return Expectations

Despite the short-term volatility, the fundamental growth rates across our Innovation Portfolio are extreme right now, and the 2026 setup is the strongest we have seen heading into the calendar year since 2023, when our Innovation Portfolio returned +98.4%.

- Track Record: Over the last three years (2023, 2024, and 2025), our Innovation Portfolio has delivered a 273.7% total return, compounding at an annualized rate of 55.25%, finishing in the top 1.32% across several thousand ETFs.

- 2026 Expectation: We continue to expect a Total Return of approximately 50% for the calendar year 2026 for the Innovation Portfolio. Given the portfolio is down roughly 10% year-to-date, this implies extreme returns from this current depressed level.

- The Setup: With the Fed expected to cut rates, valuations at historically low levels set to rebound, and AI-driven growth accelerating across software and multiple non-software industries, we expect this year to be even stronger than our +39.3% return in 2024 and +35.2% in 2025.

We are committed to our strategy of owning the companies driving the highest revenue growth across AI, software, and cloud infrastructure. This is not a time to panic, but a time to be patient and, for those who are able, to add capital at these deep discounts.

If you would like to discuss this further, please do not hesitate to reach out.

Questions? Seeking Further Insight?

Connect with our experts at BRIM.

“It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

Warren Buffet